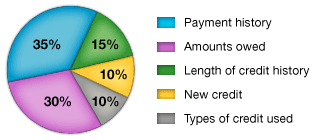

Payment History

In the payment history category, they are looking for how many accounts you have that are considered “paid as agreed.” Also, the types of accounts will be treated differently. Whether or not you have any late payments and to what degree they are late is looked at. How much is past due will factor into your score.

Amounts Owed

In the amounts owed category, how much that is owing will factor into the score. The number of accounts with balances will factor into your score, so if you have a balance on all your accounts you will get a large point deduction. Conversely, if you have no balance on all of your accounts, you will get points added to your score. One other factor that is seriously considered is the proportion of credit lines used. Anytime your credit line exceeds 30% of the balance, your score will suffer, and more points will be deducted proportionate to the percentage of total credit line that you owe.

Length of Credit History

In this category, the credit calculators will look at how long your accounts have been open. Typically, this is looked at in terms of average length per account. The longer your average length per account, the better your score will be.

New Credit

In the new credit category, your score will be affected by the number of recently opened accounts that you have, the number of recent credit inquiries, and time since last credit inquiry. If you run out and apply for many accounts at once, your score will suffer as this would suggest that you are desperate for credit.

Types of Credit

This portion of your score is based on the number of or prevalence of any one type of account whether it be mortgage, installment loans, credit cards, retail accounts, etc.

If you want a cheap way to monitor your credit score, I recommend MyFico. They will monitor your score and send you both an email and text message whenever your score changes. They also have great tools for disputing credit mistakes and so on. You can click on the link below to go to their credit monitoring info page.

Monitor Your FICO® Score & Equifax Credit Report

1 comment:

well everything is good here

Free Music

Post a Comment